GENERAL

Sodium-ion Battery Market is growing! | Three Core Tracks, Layout Combing

Introduction

Electrochemical energy storage systems can be subdivided into lithium-ion battery energy storage, sodium-ion battery energy storage, and flow battery energy storage, depending on the battery pack.

These technical routes have their own characteristics, but lithium-ion battery energy storage systems currently occupy a significant leading position in installed power.

In terms of battery performance, sodium batteries have shown their unique advantages, such as higher safety, excellent rate performance, and stable performance in low-temperature environments, and are expected to become a strong competitor to lithium batteries in the future.

From the perspective of the industrial chain, the refining process of sodium resources is relatively simple, the cost is low, and the domestic resource reserves are rich, which provides a strong guarantee for the stability of the supply chain.

In addition, in recent years, polyanion systems such as sodium iron sulfate have made significant breakthroughs in technology, which not only have good cycle performance and cost advantages, but are also expected to break the two major sodium power development bottlenecks of “downward lithium prices” and “energy storage cycle”, paving the way for subsequent large-scale mass production.

Table of Contents

Overview of the sodium-ion battery industry

The similarity between sodium and lithium in electrochemical properties makes sodium batteries an ideal alternative to lithium batteries in theory.

From the perspective of downstream application scenarios, there is a high degree of overlap in the application fields of sodium batteries and lithium batteries, especially in the fields of energy storage and low-speed electric vehicles, where their substitution potential is particularly prominent.

In addition, considering the abundant reserves and low cost of sodium salts, as well as the pressure of the current high lithium price on the industrial chain, the market demand for sodium-ion batteries is becoming increasingly urgent.

In addition, sodium-ion batteries also show obvious advantages in resources and costs, and therefore have huge application potential in fields such as large-scale electrochemical energy storage, and are likely to become a strong competitor or even a substitute for lithium-ion batteries in the future.

The working principle of sodium-ion batteries is similar to that of lithium-ion batteries. Both rely on the embedding and extraction of sodium ions between the positive and negative electrodes to achieve the storage and release of electrical energy.

The core structures of both batteries include cathode materials, anode materials, current collector, electrolyte and separator.

During the charging process, sodium ions are released from the positive electrode material, embedded into the negative electrode material through the electrolyte, while electrons flow to the negative electrode through the external circuit to ensure that the charges of the positive and negative electrodes remain balanced.

During discharge, this process is reversed. Compared with lithium-ion batteries, sodium-ion batteries have shown significant advantages in cost, safety, fast charging capability and cycle life, so they have broad application prospects in application scenarios such as energy storage systems, low-speed vehicles, two-wheeled electric vehicles and communication base stations.

From the perspective of cost composition, the main differences lie in the cathode material and the current collector.

Data from Sino-Science Sodium shows that the cost of copper-based cathode materials for sodium-ion batteries can be reduced by nearly 60% compared with lithium iron phosphate cathode materials. In addition, since sodium and aluminum are not prone to alloying reactions, the current collector can completely use aluminum foil instead of copper foil, thereby reducing costs by nearly 70%.

Sodium Battery Cathode Materials

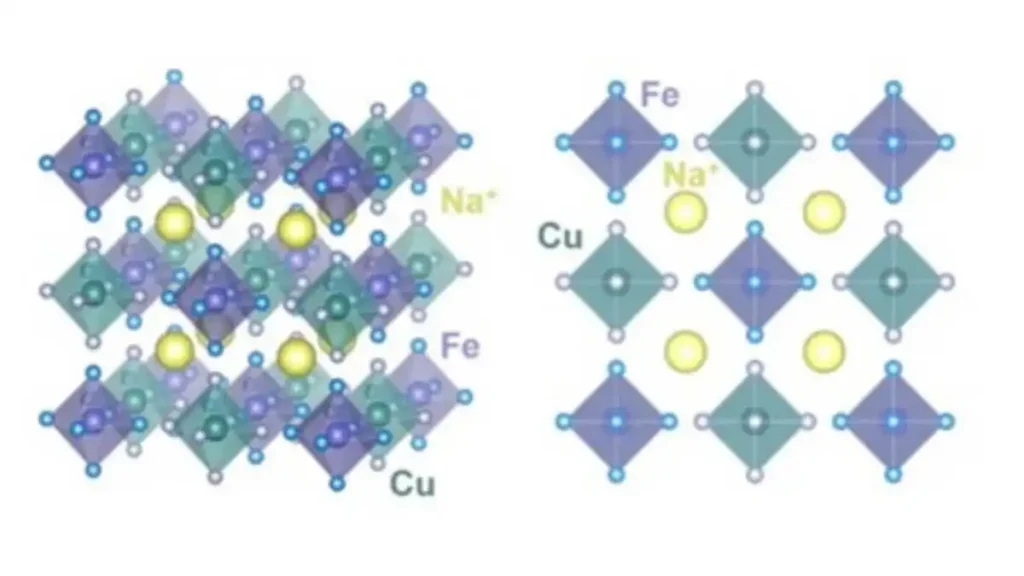

Cathode materials technology is showing a trend of diversification. At present, the positive electrode material system of sodium-ion batteries is mainly divided into three technical routes: layered transition metal oxides, polyanions and Prussian blue.

Layered transition metal oxide positive electrode materials have been the first to achieve mass production due to their advantages such as low cost, simple process and relatively mature technology.

Prussian blue materials show great potential for future development with their low cost, high specific capacity and energy density, as well as excellent rate performance.

Polyanion material system is similar to lithium iron phosphate material, with low cost, no resource restrictions, good cyclicity and safety, etc., which is very suitable for large-scale application and is expected to be widely used in the energy storage market in the future.

Sodium Battery Anode materials

Under the background of tight balance between supply and demand of lithium resources in the future, the industrialization process of sodium batteries is expected to be accelerated.

The performance of sodium-ion batteries mainly depends on their positive and negative electrode materials, among which the layout of negative electrode materials in domestic enterprises is relatively small and the price is relatively high.

At present, the cathode battery materials of sodium batteries mainly include carbon-based materials (such as soft carbon and hard carbon, etc.), alloy materials, transition metal compounds and organic compounds. Among them, the amorphous carbon process is relatively mature.

Because the radius of sodium ions is larger than that of lithium ions, it cannot be embedded/deintercalated between graphite layers. Therefore, the negative electrode of sodium-ion batteries uses amorphous carbon materials with a large degree of disorder, which are mainly divided into hard carbon and soft carbon.

The main advantage of hard carbon is its high sodium storage capacity. Its precursor is usually biomass or its derivatives, and the carbon yield after carbonization is low, so it is slightly insufficient in terms of economy.

In contrast, the advantage of soft carbon is its lower cost. Its precursor is petrochemical raw materials, and the cost is lower than that of hard carbon. In addition, soft carbon has fewer defects, its hierarchical structure is more ordered, and the interlayer spacing is shorter, resulting in relatively low sodium storage.

In the amorphous carbon negative electrode market, hard carbon occupies a dominant position, while the industrial layout of soft carbon products is relatively small, mainly dominated by companies such as Zhongke Haina.

Since 2023, the progress of sodium batteries in the application end has accelerated significantly. Electric two-wheeled vehicle brands have launched related products one after another. At the same time, multiple MW-level energy storage projects have been successfully connected to the grid and put into operation. These factors are expected to drive the penetration rate of sodium batteries into an upward stage.

With the successive participation of leading companies, the industrialization process of sodium-ion batteries has begun to advance rapidly. At the same time, the relevant supporting industrial chains such as positive and negative electrode materials and electrolytes have also been initially formed. At present, about 20 companies in China have clarified the production capacity planning of sodium-ion batteries, and the production capacity planning of some companies has reached the GWh level. By 2024, sodium batteries are expected to begin to realize industrialization.

Sodium Battery Electrolyte

In terms of electrolyte, the chemical system difference between sodium battery and lithium battery is relatively small, and most production lines can realize lithium/sodium sharing.

In China, sodium battery start-ups and traditional lithium battery companies are accelerating the implementation of sodium ion electrolyte materials.

From the perspective of the types of companies currently deploying electrolyte materials, they are mainly divided into three categories: the first category is start-ups that comprehensively deploy the entire industrial chain of sodium ion batteries, including positive and negative electrode materials and battery cells; the second category is companies with rich experience in the production of lithium battery electrolyte materials; the third category is companies whose traditional main industry chain extends to sodium ion electrolytes based on technology and application

Conclusion

At present, many companies have actively laid out the industrialization process of sodium-ion batteries, including the expansion of traditional lithium battery manufacturers into the field of sodium-ion batteries, as well as the active participation of innovative companies.

From the perspective of long-term development, the latest statistics from EVTank show that the total planned production capacity of sodium-ion battery companies has reached 275.8GWh. However, it will take some time for the sodium-ion battery industry chain to mature and achieve the theoretical low-cost level. Therefore, its large-scale industrialization application is expected to wait until 2025.

Damon Self-Ligating Braces: How They Differ From Traditional Braces

How to Evaluate a Dental Marketing Agency Before Hiring One

What Lifestyle Habits Can Help Protect Your Dental Implants for Years to Come?

Innovative Deer Control Solutions That Safeguard Gardens in Suffolk County

Back Casting Room: Definition, Setup & Best Practices

NFLBite: A Fan-Driven Hub for Free NFL Game Streams

How To Build a Back-Friendly Daily Routine In 2026

How Project-Based Learning Transforms Third Grade Classrooms

What Entrepreneurs Can Learn From the MAKE Wellness Growth Strategy

Why More People Are Choosing 1-to-1 Personal Training

Streaming Your Workouts at Home: How to Build the Perfect Fitness Setup

Social Media Scheduler Guide: Features, Benefits, Best Practices & Tools

Eagle Pose: Quick and Easy Guide

Happy Baby Pose: Benefits, Steps, and Tips for Beginners

Detoxify Your Body and Mind with Dragon Pose: A Step-by-Step Guide

-

GENERAL1 year ago

GENERAL1 year agoChristofle – For Those Who Dream of Family Heirloom Silver

-

SPORTS1 year ago

Discover the World of Football with Streameast: Watch Your Favorite Leagues and Tournaments

-

GENERAL7 months ago

Uncovering the World of кинокрадко: The Dark Side of Film Piracy

-

GENERAL4 months ago

Unveiling the Art of преводсч: How Translators Bridge Language Barriers